Working with income

In order to pay your expenses, pay down your debts, and so on, you need to have money coming in. That's your income, which you fill out here.

Please note that any income you anticipate, you should fill in here. If your buddy owes you $500 and is going to pay you next month, then add it in! If you always get $50 from your grandmother on your birthday, add it in! If it's money coming in, you should add it in. If you don't, then Debtinator won't be able to use it when generating scenarios for you, which could cost you money in the long run.

Please note that an expense is considered something that's fixed, or at least reasonably fixed. Your rent doesn't vary from month to month, your cable bill doesn't change, your cell phone bill is probably constant. Some of the money you spend goes to unfixed things, like food or gas or movie rentals. Setting up a fixed expense for those items isn't quite accurate, since it's not like you write a check for $20 to the video store each month for your rentals. Instead, you should segment your account with virtual budgets to set aside money to fund these activities. See Setting up budgets for more info.

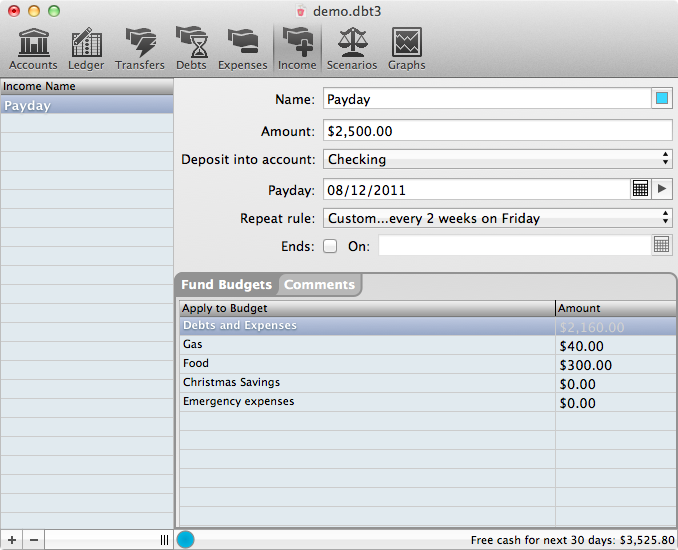

- Name - The name of the expense in question. "Rent", "Cable bill", etc. Next to the name is a color well so you can color code this expense.

- Amount - The amount of the expense.

- Deposit into account - The bank account you deposit this money into.

- Payday - The next date you'll receive this income

- Repeat rule - how often this income occurs. See Editing Dates for more info

- Ends - If you don't want this income to continue on forever, you can stop it here

- On - and specify the date that it ends

- Apply to Budget - By default, all of your income goes towards your debts, but here's where you can segment it into the budgets you've defined for your account. In this case, we get paid $2,500 every other Friday. We keep $2,160 to fund our debts and expenses, set aside $300 for food, and $40 for gas. We've set up budgets to save for Christmas and Emergencies, but we're not actually setting aside any money for them right now. See Setting up budgets for more info.

To work with income:

- Click on the income button in the toolbar.

- Click the '+' button in the lower left, or select an income event and hit the '-' to delete it.

- Fill in the income information.