Get your debts under control

Everybody always tells you that you should get out of debt. Now. Fast. As fast as you can. Think of the money you'll save!

But...realistically? So what. Talk, talk, talk. You've got bills to pay. You've got a life to live! You have expenses. Sure, you'll try and send the occasional $50 to your student loan from time to time, when you can. But if you happen to miss a few of those, well, what's the harm? It'll be paid off eventually, right?

It's incredible how fast that adds up. How those occasional times you don't pay a little extra turn into frequent events. How your debt tends to stay at the same high level it's always been, or even worse - goes up. How you can always tell yourself that it's okay, because you can worry about paying it all down tomorrow.

Well, it's tomorrow.

Getting out of debt is like going on a diet - sure, you know the basic idea: spend less than you earn. Just like to lose weight you just need to burn more calories than you eat. Ahh, but the tricky part is that it's so much easier to get into debt than out of it. It's so much easier to give in and eat the whole cheesecake than to worry about all the calorie counting you're going to need to do to make up for it. Let's face it, you can't impulse buy your way out of debt. You need a plan. You need strategy.

Frankly, "one size fits all" approaches of saying that you shouldn't go out to eat any more or should never buy a new video game just don't work for most people. We don't have any clue how you want to live your life. But you do! You know how much you want to spend on living your life now. Sure, retirement savings is important, but so is getting out of debt. But it can't be done at the expense of the rest of your life or you'll never stick to the plan. Tell Debtinator how you want to live your life and it'll work within those parameters to give you a faster pay-off strategy than you realized you could accomplish.

That's how you succeed when other plans fail. We're not one size fits all. We're not worried about where you've been in the past or what you spent money on last week. That's like driving down the highway by only looking in your rearview mirror. We want you to think about where you're going. Come up with a plan of how to live and what's important to you. Then we'll help fill in the gaps for you to knock out your debt lightning-fast while maintaining what you want to be.

What if it turns out that you can't live that way? That your lavish lifestyle won't leave enough money to cover your bills? Then we'll tell you that, too. So you know now that you can make changes and can figure out what to cut back on.

Or maybe you'll want to cut back on it anyway. Play around with the numbers to see what works for you. Maybe if you ate out one fewer time per month, then you'll be out of debt 6 months earlier. Is that worth it to you? It's your decision - but you can see the number and see the effect. Sure, it's nice to have dinner on the town, but you can also see the repercussions to decide if it's really worth it to you in the long run.

All Debtinator cares about is where the money is coming from and where it's going to. It'll do its best to get you out of debt as fast as possible, by saving you as much interest as it can. But it's up to you to prioritize whether you want to have more fun now or save more money in the long term. But without the numbers and information that it provides, you can't make an educated decision.

How does it work?

Debtinator looks for the money that falls through the cracks. Sure, you set up your income and expenses and budgets, but chances are you're using nice round numbers. So there's a little bit extra left over at the end of the month. You may have $1,000 in income, but only $950 in expenses. The trick is putting that extra $50 to work for you, because otherwise, it's just wasted.

That little bit of money is what we all tend to waste. That's the stuff you look at and say, "Hey free money! I'm ordering a pizza!" and then it's gone as soon as you found it. The thing to remember is - you didn't even know you had it, so you're not going to miss it. You've already set aside the money that you want to spend. So you have your video games and pizza and night at the movies. You've already planned for it, this is just something extra. So instead of getting just one more pizza, you use it to pay a little more to your debt.

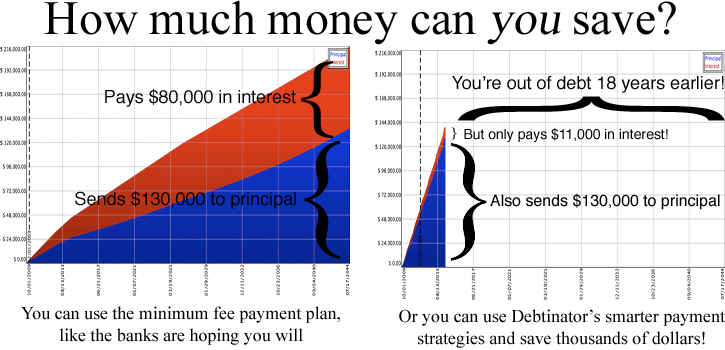

It just snowballs from there. Every spare cent Debtinator finds gets paid to your debts. As debts get paid off, that frees up more money to send to other debts, which get paid off faster, which frees up more money, and on and on and on. You can quite literally save thousands of dollars.

But why not just do it myself?

People like to try and send a little bit extra "when they can." And that's fine, but it's inefficient. Debtinator sends all the money you can afford and won't miss to your debts. Plus, it's smart enough to plan for the future. So you can say that you may try to send an extra $100/month, but maybe you actually shouldn't. What if you send an extra $100 each month, but that means that you don't have the money on hand to pay for your car insurance in 6 months? Or your property tax at the end of the year? Or your child's college tuition in 10 years? It's not enough to send a little extra when you can - that's paying down your debts, but it's not planning for your future. That's where Debtinator comes in.